There’s a good chance your health insurance premiums are going up next year, regardless of where you get coverage.

Why it matters:

The spike in what millions of Affordable Care Act plan enrollees pay will be acute, but workplace insurance is getting more expensive, too — and all at a time when affordability is prominently on Americans’ minds.

ACA premiums have dominated the political discourse in Congress for weeks, but there’s no real sign that any relief is coming from Washington.

Even extending the Biden-era enhanced ACA subsidies — which most Republicans don’t want to do — would do nothing to address what’s driving the surging cost of care or employer insurance affordability issues.

And all signs point to Democrats hammering Republicans for high costs in all forms of health insurance leading up to next year’s midterm elections.

The big picture:

Health insurance gets more expensive almost every year, keeping up with increases in the costs of procedures, tests, drugs and more. But some years see bigger jumps than others, and 2026 is looking like one of those years.

That means tough choices for families, employers and workers all faced with shouldering higher premiums or out-of-pocket spending. Some will conclude it’s prohibitively expensive and go uninsured.

Another thing that’s different about this year is that the white-hot political rancor around ACA premiums is putting health insurance back centerstage politically.

By the numbers:

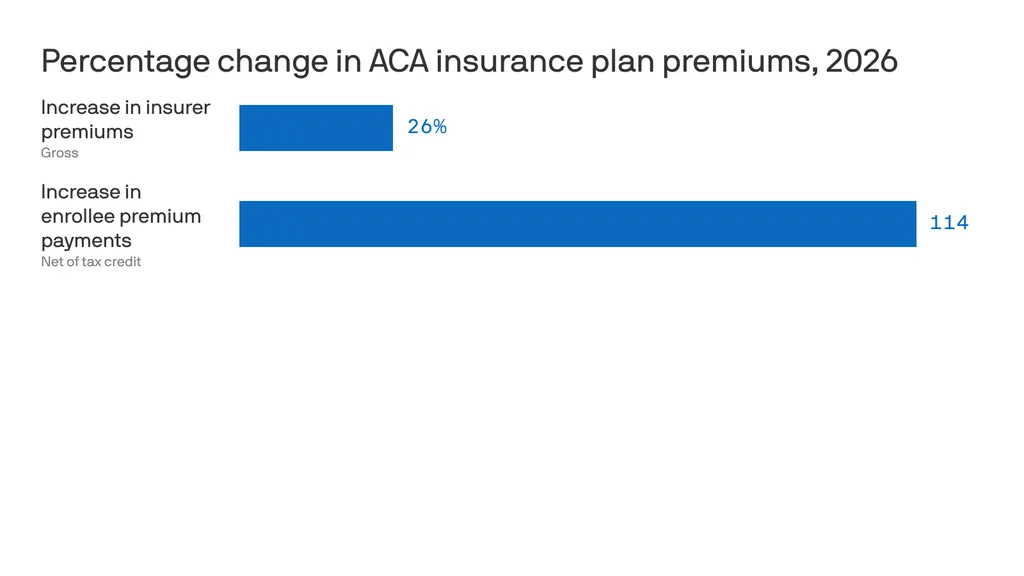

ACA insurers themselves are raising premiums by an estimated 26%, in part due to rising hospital costs, higher demand for pricey GLP-1 drugs like Ozempic, and the threat of tariffs.

But add in the loss of federal subsidies, and the increase is 114% — or more than double what they currently pay, according to KFF. 22 million out of 24 million marketplace enrollees now receive subsidies.

Premiums in the small group employer market will go up by a median of 11%, also per KFF, due to some of the same reasons insurers cite in ACA markets.

For employer health insurance, there’s no comprehensive data yet for 2026, but estimates from earlier this year put the increases in the high single digits.

For example, according to Mercer, health benefit costs are expected to increase 6.5% per employee in 2026, and many employers are planning to limit premium increases by raising out-of-pocket costs for employees.

One factor driving these increases is advances in medicines, like new cancer treatments, that are more expensive, according to Mercer.

But people are also using health care more, per Mercer. That’s possibly because they missed or delayed care during the pandemic — but also because the use of AI in doctors’ offices gives them more capacity and allows them to work faster.

Between the lines:

Just this month, Gallup polling found that approval of the ACA has hit an all-time high of 57%, including more than 6 in 10 independents but only 15% of Republicans.

Another recent Gallup poll found that 29% of Americans say that cost is the “most urgent health problem” facing the country, up from 23% a year ago.

The bottom line:

Get ready to hear a lot more about health care costs over the next year — while potentially also experiencing your own premium increase.

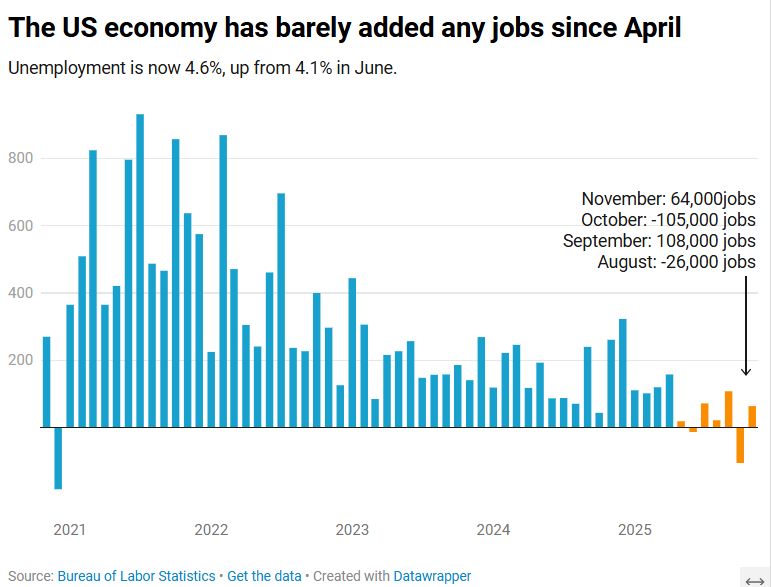

The US economy added 64,000 jobs in November, according to the Bureau of Labor Statistics.

The US economy added 64,000 jobs in November as the unemployment rate crept up to 4.6%, according to Labor Department data published Tuesday.

The unemployment rate is now at its highest level since September 2021.

The November jobs report, originally scheduled to be published Dec. 5 before the 43-day government shutdown delayed multiple economic data releases, comes as Americans stress over rising layoffs and a frozen job market that can feel impossible to break into. Tuesday’s report suggested those conditions persisted toward the end of the year.

Economists surveyed by Bloomberg had expected a gain of 50,000 jobs. The healthcare sector, which has fueled job growth this year, added 46,000 positions for the month.

November’s data additionally showed that the number of people employed part-time for economic reasons rose to 5.5 million in November, an increase of 909,000 over September. Meanwhile, the long-term unemployment rate, or the share of unemployed people who have been without jobs for 27 weeks or more, was 24.3% in November, down from August’s high of 25.7% but higher than the rate of 23.1% seen a year ago.

“The US economy is in a hiring recession,” Heather Long, chief economist at the Navy Federal Credit Union, wrote in a post on X.

“Almost no jobs have been added since April,” Long added. “Wage gains are slowing. 710,000 more people are unemployed now versus November 2024.”

Nancy Vanden Houten, lead US Economist at Oxford Economics, said in a statement that the government shutdown appears to have contributed to the increase in the unemployment rate.

“The number of permanent job losers, which had been ticking higher, declined. Labor force growth also contributed to the increase,” she said.

Partial data for October, also published Tuesday, showed a loss of 105,000 positions. The unemployment rate for the month will not be released. Bank of America economist Shruti Mishra had noted that October’s payroll numbers would be affected by the delayed impact of DOGE-led government job cuts, since many federal employees who opted for the “deferred resignation program” officially left their positions Sept. 30.

The federal government lost 162,000 jobs in October and 6,000 in November, according to the Labor Department.

Forbes last month released its second-annual “America’s Best Companies” list, recognizing 500 companies, including 44 healthcare companies — several of which are Advisory Board members.

For the list, Forbes looked at public and private companies as well as foreign-based companies with a U.S. subsidiary and analyzed more than 100 metrics across 11 categories. Companies with U.S. headquarters that employ more than 7,000 people in the United States were eligible for the list.

The primary categories Forbes looked at, and the data partner it worked with, were:

Employee sentiment (Glassdoor), where workers rated their company in categories like career opportunities, compensation and benefits, and confidence in senior leadership.

Customer sentiment (HundredX), where consumers rated products they purchased in categories like customer service, value, and dozens more.

Financial performance (Forbes), which looked at one- and five-year metrics for stock prices and revenue growth.

Business trajectory (Crunchbase), which assessed metrics that consider dozens of financial indicators like funding, market share and movements, and company growth.

Cybersecurity (SecurityScorecard), which assessed categories like network and applications security, malware vulnerability, and regularity of patches.

Media sentiment (SignalAI), which reviewed positive and negative company coverage of executive leadership, innovation, diversity performance, and financial performance.

Workforce diversity (Denominator), which assessed representation at both executive and lower levels of the company of different groups, including gender, race/ethnicity, age, education, disability, and nationality.

Sustainability (Morningstar), which assessed the robustness of climate governance, sustainability strategy, risk management, and financial and competitive strength.

Workforce stability (People Data Labs), which looked at each company’s workforce growth rate, churn rate, and average C-suite tenure.

Company size (Data Axle), which looked at each company’s number of U.S. employees.

Each company received an individual category score that was normalized and adjusted where appropriate to reflect how that score compared to competitors in their sector. Those scores were then combined to create a final score to develop the rankings.

The best healthcare companies in the US

In the drugs & biotechnology industry, the companies recognized on the list were:

87. AbbVie* (Chicago, IL)

119. Johnson & Johnson* (New Brunswick, NJ)

164. Amgen (Thousand Oaks, CA)

235. Gilead Sciences (Foster City, CA)

280. Merck & Co. (Kenilworth, NJ)

394. Thermo Fisher Scientific (Waltham, MA)

460. Zoetis (Parsippany, NJ)

477. Biogen* (Cambridge, MA)

*Denotes an Advisory Board member

In the healthcare equipment & services industry, the companies recognized on the list were:

146. GE HealthCare Technologies (Chicago, IL)

331. Ansell Healthcare (Iselin, NJ)

357. Alcon Vision (Fort Worth, TX)

384. Henry Schein* (Melville, NY)

395. Herbalife International of America (Los Angeles, CA)

409. Home Life Care (Ahoskie, NC)

415. Zimmer Biomet* (Warsaw, IN)

422. Smith & Nephew (Memphis, TN)

442. Chemed (Cincinnati, OH)

443. Encompass Health* (Birmingham, AL)

497. Merrill Gardens (Seattle, WA)

*Denotes an Advisory Board member

In the healthcare & social services industry, the companies recognized on the list were:

45. CVS Health (Woonsocket, RI)

275. Northside Hospital* (Atlanta, GA)

309. Main Line Health* (Radnor Township, PA)

374. Oklahoma Heart Hospital (Oklahoma City, OK)

452. Sharp HealthCare* (San Diego, CA)

464. Carle* (Urbana, IL)

468. Henry Ford Health System* (Detroit, MI)

469. Sutter Health* (Sacramento, CA)

475. Virtua* (Marlton, NJ)

484. Cincinnati Children’s (Cincinnati, OH)

492. Harris Health System* (Houston, TX)

*Denotes an Advisory Board member

In the medical equipment & services industry, the companies recognized on the list were:

44. Abbott Laboratories (Chicago, IL)

103. Boston Scientific* (Marlborough, MA)

121. Dexcom* (San Diego, CA)

152. McKesson* (Irving, TX)

200. Intuitive Surgical (Sunnyvale, CA)

219. Stryker* (Kalamazoo, MI)

250. Labcorp Holdings* (Burlington, NC)

286. Cardinal Health (Dublin, OH)

342. Agilent Technologies (Santa Clara, CA)

347. Becton Dickinson* (East Rutherford, NJ)

425. National Vision (Duluth, GA)

436. Quest Diagnostics* (Secaucus, NJ)

*Denotes an Advisory Board member

In the pharmacies industry, the companies recognized on the list were:

Next year, seniors and families will have more stringent and more unaffordable health coverage thanks to new AI-driven prior authorizations in Medicare and loss of subsidies in the ACA.

The New Year is just two weeks away, and when Americans wake after clinking champagne and kissing at midnight, the health care landscape in the United States will be in worse shape than it was in 2025. There is a growing list of why that’s true, but here are a couple of developments that will make it harder for many of us to get the care we need:

The December 31 expiration of the Affordable Care Act enhanced subsidies, which will lead to millions of Americans losing coverage and make premiums barely affordable for millions of others; and

CMS’s January 1 implementation of a new pilot project that will put private, for-profit contractors using AI-powered prior authorization in traditional Medicare.

Unless policymakers change course, many Americans will be ringing in 2026 with higher costs, less access and a nasty health care hangover.

WISeR strikes at 12

As we’ve reported, the implementation of the Wasteful and Inappropriate Service Reduction (WISeR) model’s will mark the first time in traditional Medicare’s 60-year history that for-profit companies will decide whether seniors receive certain medical services their doctors recommend. Six companies — many with deep ties to Big Insurance and insurer-backed venture capital — will suddenly have the power to say yes or no to 17 procedures that never required prior authorization before. And for these companies, the more the denials, the bigger the profits.

As Dr. Seth Glickman documented after sitting through CMS’s own WISeR webinar, the rollout has been vague on details and confusing to providers and patients. CMS even admitted during the webinar that the vendors chosen to administer the model were selected in part based on their “success” of using prior authorization in the private Medicare Advantage program, which is notorious for denials, delays and life altering decisions.

Some lawmakers in Washington have taken notice. A coalition of Democrats introduced the Seniors Deserve SMARTER Care Act, warning that WISeR creates “a dangerous incentive to put profits ahead of patients’ health.” Imposing prior authorization in traditional Medicare “will kill seniors,” said Rep. Mark Pocan, one of the bill’s sponsors.

Kiss subsidies goodbye

While WISeR threatens seniors’ access to care, millions of working families are facing a different New Year’s surprise: the expiration of enhanced ACA marketplace subsidies, which Congress has (so far) failed to extend or replace. As Rachel Madley, PhD wrote in October, families will have to gamble when they pick a health insurance plan. She added:

The enhanced premium subsidies being debated in Congress right now are a lifeline for so many of us and must continue in the short term, but they don’t fix the underlying problem: Private insurers extract value rather than control costs or provide access to necessary and affordable care. Decades of experience show that when profits rule health insurance, families face financial ruin no matter which plan they pick during open enrollment.

But as we’ve noted before, this isn’t an existential crisis for Big Insurance. ACA marketplace plans are not where insurers make their real money. Their profits flow increasingly from taxpayer-funded programs like Medicare Advantage and Medicaid managed care — the same universe WISeR is quietly expanding.

One proposal to “solve” the subsidy issue, endorsed by President Donald Trump and HELP Chairman Bill Cassidy, would not extend the tax credits but put $1000 to $1500 into government-sponsored health savings accounts (HSAs). HSAs can be helpful if you you have crappy insurance – or are rich and need an additional place to put your money to avoid taxes – but not a meaningful solution to the millions of Americans facing a 75% hike in premiums or finding themselves priced out of coverage altogether in 2026. The supporters of this approach claim it would somehow take money away from health insurers, but it would just reroute federal dollars to those same companies. For instance, UnitedHealth Group, which owns the nation’s biggest HSA custodian, could grab even more of our tax dollars than they already do. Meanwhile, families would still be exposed to unaffordable premiums and massive out-of-pocket costs. Champagne dreams.

Thanks to these changes in health care: The hangover on January 1, 2026, won’t only be from the previous night’s festivities – and it won’t be cured with some water and Advil. Cheers.

The OIG found that Anthem paid its own corporate sibling as if it were an outside vendor. The maneuver transformed a cost-based function into a source of “unlimited profit.”

When the Office of Inspector General (OIG) audited Anthem Blue Cross and Blue Shield insurance plans for federal employees recently, auditors appeared to be conducting a typical contract compliance review.

While they may not have been looking for a smoking gun, they stumbled upon one.

At first glance, the report on Elevance Health’s Anthem Blue Cross and Blue Shield insurance under the Federal Employees Health Benefits Program (FEHBP) looks like just another technical review, questioning charges and payments across familiar audit categories such as uncollected claim overpayments, administrative expense overcharges, medical drug rebates, provider offsets and lost investment income. The auditors’ stated goal was to “obtain reasonable assurance” that Anthem was complying with contract terms. The review took a turn from the routine when the OIG looked at how Elevance is using a common insurance practice known as subrogation.

The issue of subrogation emerged after the OIG observed irregularities in recoveries and fees being passed through the plan. Subrogation – recovering costs from insurers, auto carriers or liable third parties – is a familiar function. But the structure Anthem created is not.

Anthem Inc. became Elevance Health Inc. in 2022 and also launched Carelon health services. Elevance became the name of the parent company, but the name Anthem was retained for the health plans the company operates across the country. Carelon, a wholly owned Elevance subsidiary, is a corporate sibling of the Anthem health plan division, and it’s the fastest-growing of the two. In fact, Elevance views Carelon as the company’s profit engine.

The OIG discovered that Anthem treated Carelon as a commercial provider of services in an arm’s length transaction and paid Carelon a percentage of recoveries, even though, as OIG wrote, this was a “related party transaction.” Auditors discovered that Anthem had contracted its subrogation work to Carelon, and then billed the FEHBP a percentage-based “fee,” deducted directly from the recoveries, and recorded it as a health benefit expense rather than an administrative cost. The subrogation fees then passed through FEHBP as medical claims, thereby avoiding oversight limits on administrative costs and creating “unlimited” profit on a function that should have been cost-based.

Self-enrichment

The OIG was especially troubled because the transaction was a “related party transaction,” which in government contracting is the polite way of saying you’re paying yourself. Worse, the OIG found that:

“The method Anthem uses to charge these subrogation recovery fees results in unlimited profits for essentially an ‘in-house’ service…

And that:

“Elevance Health, Anthem, and/or Carelon should not benefit or self-enrich at the expense of the FEHBP.”

The auditors also concluded that:

“… the only profit that can be charged to the FEHBP is the negotiated annual service charge…”

But Anthem had charged $39,235,156 in subrogation fees plus $5,638,360 in lost investment income – exactly the kind of profit the contract prohibits.

What’s most shocking about this audit isn’t what Anthem did – it’s how openly they did it, and how little anyone plans to do about it.

To appreciate the magnitude of the audit discovery, it helps to understand how the Federal Employees Health Benefits Program actually operates – and who really runs it. The FEHBP is a roughly $70billion annual program covering more than eight million federal workers, retirees and dependents. Yet the federal government does not administer these benefits directly. Instead, it contracts with the Blue Cross Blue Shield Association (BCBSA), which then delegates day-to-day administration to individual Blue plans across the country.

Among those plans, Anthem administers services in 14 states – more than any other Blue plan – and during the audit period was responsible for $40.6 billion in FEHBP benefit payments and $2.1 billion in administrative expenses. Anthem isn’t simply one contractor in a crowded field; it is the dominant operational arm of the BCBSA for a vast portion of the federal population. When Anthem selects a vendor, sets payment terms or withholds documentation, it is not a peripheral actor – it is effectively shaping how the federal health plan functions.

What’s worse than getting caught red-handed breaching the contract? The company’s response. Its posture throughout the report is equal parts dismissive, pedantic and openly defiant. It insisted the fees represented “allowable, commercially reasonable charges,” argued that subrogation was a “commercial service,” and maintained that the costs were “not subject to cost analysis.”

The company repeatedly pushed back with formulations that would seem to suggest that Elevance itself, and not the OIG, was the final authoritative voice on contract compliance and legality:

“We disagree with the OIG’s characterization.”

“We do not concur.”

“The services are allowable and reasonable in view of the commercial marketplace.”

When the OIG pressed for documentation to substantiate these so-called “commercially reasonable” fees, they were met with outright refusal. They were told that no such documentation existed. Unfortunately for Anthem, they proved themselves wrong in a meeting with OIG when they inadvertently displayed a detailed spreadsheet showing a cost analysis for corporate subrogation services – the very spreadsheet the company had insisted did not exist. As the OIG noted:

“Anthem inadvertently shared an Excel spreadsheet which included the total corporate Carelon subrogation costs by year – precisely the cost data we have been requesting.”

Rather than simply hand it over, the company declared the spreadsheet “not accurate,” “not relevant,” and “not responsive.”

It gets worse. When the auditors asked for a valuation prepared by the company’s accounting firm, Deloitte – the same valuation Anthem itself relied upon as proof that they had studied the reasonableness of their charges – the company responded by producing six heavily-redacted pages out of a 900-page report. That’sless than 1% of the analysis they claimed fully justified their pricing, which costs the FEHBP over $40 million.

The OIG, in its dry bureaucratic tone, noted that the company’s justification for withholding “over 99 percent of the Deloitte study” was “insufficient” – which is government-speak for, “Are you kidding me?” The OIG all but throws up its hands:

“We cannot determine the actual profit charges and/or the reasonableness of these fees due to the scope limitation created by Anthem’s refusal to provide documentation access.”

Anthem behaves as though the worst that can happen is that someone at OIG writes a sternly worded paragraph in a report that will sit unread on a government website. Unfortunately, they are probably right.

As the OIG delicately put it:

“Throughout the audit process, we encountered numerous instances where Anthem responded untimely and/or initially provided incomplete responses.”

And why would Anthem cooperate? The OIG report is unlikely to trigger meaningful enforcement, the federal Office of Personnel Management has historically acted more like a deferential plan sponsor than a regulator, and Congress appears largely uninterested in disrupting a status quo that serves the BCBSA and its licensees quite well.

62% profit margin

Ultimately, due to the lack of information from Anthem, OIG acknowledged that it was forced to estimate the degree of unallowable profit. Based on the limited corporate subrogation cost data they could see, auditors concluded that Anthem was likely earning a profit margin of approximately 62%.

Think about that: a federal contractor potentially earning a 62% profit margin on a supposedly in-house function, inside a federal health plan that legally prohibits this form of profit.

Discovery of a profit extraction model

All of this is visible only because the OIG happened to expand a limited audit sample into subrogation recoveries. The OIG did not enter the process intending to uncover a profit-extraction model. But it found one.

Which raises the question: what would the numbers look like if OIG examined all subrogation? Or payments for all Carelon services? Or fees related to recovery services, out-of-network negotiation and payment integrity? Or medical management? Or pharmacy recoveries?

The answers are not in the report.

What this audit shows is not just that Anthem crossed a line. It shows that those running the FEHBP lack the power, or the will, to draw one. If a contractor can profit in violation of the contract, get caught, and then simply withhold the evidence and declare they disagree, then the rules are performative and enforcement is imaginary. Anthem’s response – dismissing the OIG’s findings, withholding a 900-page Deloitte report, refusing cost documentation, and asserting a legal right to decide what data the government may review – reflects not caution, but confidence.

Confidence that there will be no consequence. Confidence that the FEHBP cannot or will not act. And, perhaps most troubling, confidence that the American taxpayer will never know the difference.

The contractor knowingly violated profit limits, hid the margin inside claims, refused to provide cost data, and continues billing unchanged. If this is what turns up accidentally, just imagine what would be exposed if anyone actually went looking.

Chris Deacon, JD, is a health care executive and consultant recognized for her advocacy for transparency and accountability. She previously ran New Jersey’s public sector health plan, covering 820k lives.

A striking thing about this week’s flow of news out of the Federal Reserve is how normal it was — at least compared to some of the possibilities that appeared in play last month for a breakdown in the institution’s longstanding norms.

Why it matters:

In the Fed’s decision to cut interest rates on Wednesday, and the unanimous reappointment of 11 of 12 reserve bank presidents announced yesterday, it was clear that Powell has retained his ability to steer a seemingly fractious organization toward consensus.

The next chair may yet shift the institution toward a process with more open dissent and count-the-votes proceduralism, as is seen at the Bank of England and as some Trump associates have advocated.

But for now, Powell looks clearly in charge despite lame-duck status (his term is up in May).

State of play:

Just a few weeks ago, it looked plausible that there would be the most open dissent from the Fed’s December interest rate decision in decades. Five officials of 12 Federal Open Market Committee voting members had expressed significant reservations about a rate cut.

Three officials who were publicly skeptical of cutting rates further — reserve bank presidents Susan Collins (Boston) and Alberto Musalem (St. Louis), and governor Michael Barr — elected to follow the leader when it was time to cast their vote.

While there were three dissents — two opposing the cut, one favoring going further — that’s not terribly abnormal. There were three dissents in September 2019, for example, also in opposite directions.

What they’re saying:

“After the high drama/psychodrama from the October press conference onwards, the end result was more business-as-usual on the part of the Powell Fed,” wrote Krishna Guha and colleagues at Evercore ISI in a note.

In his news conference, “Powell was calm and poised, not on the ropes as in October, with a governance crisis averted,” they wrote.

The big picture:

Fed watchers were braced for the possibility that the every-five-years process of reappointing reserve bank presidents would generate fireworks, an opportunity for Trump-appointed governors to try to create some upheaval at the Fed (or at least make some noise).

It came and went yesterday without signs of public dissent, as the board announced that 11 of 12 reserve bank presidents had been reappointed with “unanimous concurrence” by members of the Board of Governors.

Not only were the 11 officials re-upped, the three Trump-appointed governors did not object.

The odd man out, Atlanta Fed president Raphael Bostic, had previously announced his retirement at the end of his term in February. But one bank president stepping down at the end of a term is not unheard of; it last happened at the end of 2015 with Minneapolis Fed president Narayana Kocherlakota.

Between the lines:

On paper, the Fed chair holds only one vote out of seven on the Board of Governors and one of 12 on the FOMC. Their ability to lead the institution depends on a mix of hard and soft power.

In the hard power department, the chair oversees the staff and sets meeting agendas. In the soft power department, they must persuade their colleagues to line up with the policy path they believe is correct.

Powell has been skilled at using both — and displayed those skills this week.

There’s likely to be one more round of health care votes in the House next week after the Senate votes down two rival Affordable Care Act subsidy proposals Thursday — but they won’t get any closer to extending the enhanced subsidies.

Why it matters:

Those subsidies now appear certain to expire at the end of the year, short of a last-minute breakthrough — and out-of-pocket premium costs will more than double on average for roughly 20 million ACA enrollees.

Driving the news:

The Democratic proposal that will get a Senate vote Thursday would extend the enhanced subsidies for three years, while the Senate GOP proposal would not extend the subsidies but instead provide money for health savings accounts.

Both will fail to get the needed 60 votes.

Senate Majority Leader John Thune (R-S.D.) has left the door open for further bipartisan talks after both votes fail, but there is deep skepticism in both parties that any such deal is possible.

Sen. Tim Kaine (D-Va.) said it’s possible there is “additional discussion” after the failed votes, but said the issue also might end up in a “political solution in November when people pick the side that’s for them.”

The latest:

House GOP leaders outlined a range of possible health care options on Wednesday morning, but they have little to do with the subsidies, which weren’t included in their plans.

GOP leaders will bring “consensus” bills to the floor next weekthat aim to lower health care costs, a source who attended House Republicans’ Wednesday morning conference meeting told Axios.

Those could include expanding health savings accounts and association health plans, which allow employers to band together to purchase coverage.

Overhauling pharmacy benefit managers with the goal of lowering drug costs was also discussed, along with funding ACA payments known as cost-sharing reductions (CSRs).

The intrigue:

On the House side, a bipartisan group of moderates including Reps. Brian Fitzpatrick (R-Pa.) and Jared Golden (D-Maine) filed a discharge petition, a procedural move to force a vote on a compromise extension plan.

But that effort to go around House GOP leadership faces long odds against getting the required majority of the chamber to sign on.

Modifications to the subsidies in that plan designed to win over GOP votes, like a crackdown on zero premium plans that backers say fuel fraud, could lose Democratic support due to concerns about coverage loss.

Democratic leaders havebeen focused on a clean three-year extension, saying that is the clearest way to address the issue with little time remaining to implement changes before the new coverage year starts Jan. 1.

House Democratic Leader Hakeem Jeffries (N.Y.) told reporters Wednesday he has no position on the discharge petition.

The bottom line:

There is also deep resistance to a subsidy extension among many Republicans.

Thune has said he thinks Democratic leadership is more interested in a “political messaging” vote this week than in entertaining reforms to the subsidies that Republicans point to.

Even if members in either chamber are able to make progress on a consensus compromise subsidy plan, which in theory could be attached to a government funding bill needed before Jan. 30, the divisive issue of abortion hangs over all of the discussions.

Many Republicans insist on new limits preventing the subsidies from going to insurance plans that cover abortion. Democrats say that is a dangerous expansion of safeguards that already require taxpayer funds to be segregated and not pay for abortion coverage.

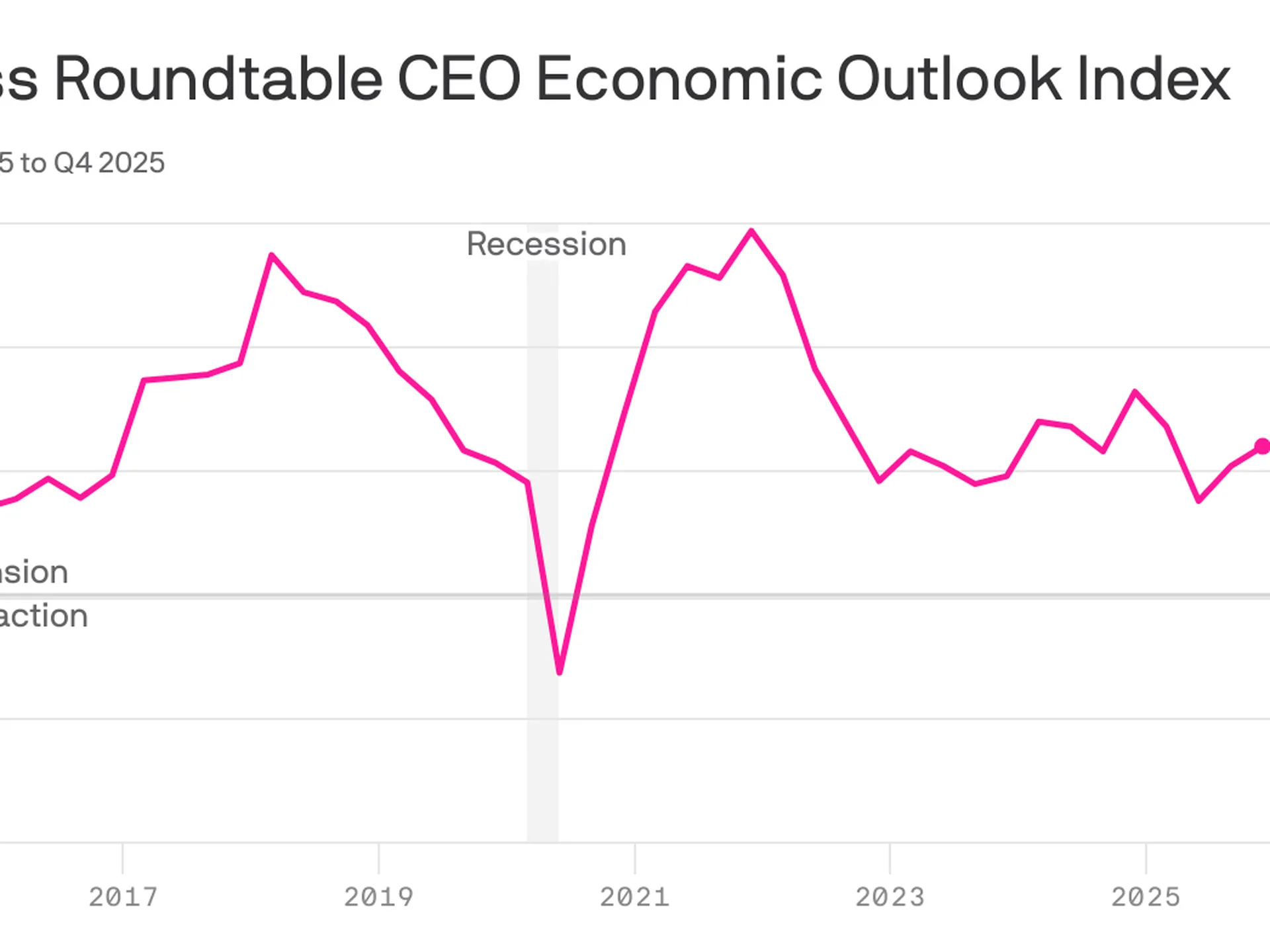

CEO sentiment increasedfor the third consecutive quarter, even as America’s most prominent executives expect underlying job market conditions to remain weak.

Why it matters:

The economic outlook among CEOs has steadily improved since plunging in the aftermath of President Trump’s initiation of the global trade war.

Under the hood, however, there is evidence that structural economic changes — including the proliferation of AI — are weighing on hiring intentions, a warning sign for the labor market.

By the numbers:

The Business Roundtable’s CEO Economic Outlook Index rose by 4 points in its fourth-quarter survey, which was fielded from the final weeks of November through earlier this month.

The index is still shy of the highest level of the Trump 2.0 era and slightly below the historical average of 83.

Zoom in:

The increase reflects a more upbeat view of company revenue in the next six months: Expectations for sales rose 6 points, though the survey does not ask respondents to adjust for the prospect of higher prices.

Plans for capital expenditures — investments in equipment, buildings or software — ticked up 2 points, following a 10-point surge in the previous quarter.

Hiring plans also improved relative to last quarter — up 4 points — though it is the survey’s lone indicator below the level that signals growth.

What they’re saying:

“Notably this quarter, more CEOs plan to reduce employment than increase it for the third quarter in a row – the lowest three-quarter average since the Great Recession,” Business Roundtable CEO Joshua Bolten said in a statement.

About one-quarter of CEOs say they will increase hiring, while 35% say employment will shrink at their respective firms. The remaining 40% plan to keep hiring steady.

A smaller share of CEOs plan to slash workers relative to last quarter, but the figures still show a notable shift among top executives.

Consider the results from this time last year: A similar share of CEOs expected no change in employment levels, but just 21% said they anticipated cutting jobs, while 38% planned to increase hiring.

“CEOs’ softening hiring plans reflect an uncertain economic environment in which AI is driving sizeable [capital expenditures] growth and productivity gains while tariff volatility is increasing costs, particularly for tariff-exposed companies, including small businesses,” Bolten said today.

The big picture:

The in-the-dumps hiring plans signaled by big firm CEOs — alongside a string of layoff announcements in recent months — signal a possible shift for the steady-state labor market that has persisted in recent years.

Powell raised the possibility that the labor market might be even weaker than government data suggests.

The economy has added a monthly average of 40,000 payroll jobs since April. But “we think there’s an overstatement in these numbers, by about 60,000, so that would be negative 20,000 per month,” Powell said at yesterday’s press conference.

“The labor market has continued to cool gradually, maybe just a touch more gradually than we thought,” he added.

The bottom line:

CEOs feel more optimistic, though that confidence boost is not expected to translate into more hiring — an unusual dynamic for the economy.

“Although the results signal that CEOs are approaching the first half of 2026 with some caution, they are starting to see opportunities for growth,” Cisco CEO Chuck Robbins, who chairs the Business Roundtable, said in a statement.

“With the Index near its average, it reflects the resilience of the U.S. economy,” he added, citing pro-growth tax policies and fewer regulations.